ISO 20022 for Securities Settlement — The sese Message Set

- What sese does

- The settlement instruction

- The settlement lifecycle

- Securities financing

- Transfers

- Settlement discipline and buy-in

- Conclusion

- Annex — Key Terms

- Frequently Asked Questions

- References

When a securities trade is agreed, nothing has really happened until the securities move from seller to buyer and the cash moves the other way. That final step, at a central securities depository or a custodian, is settlement, and ISO 20022 models it in the sese business area. This is where the earlier stages land: a clearing obligation, a collateral delivery, an FX-funded purchase all end in a sese settlement instruction. This article walks through the area’s core settlement lifecycle, its securities-financing and transfer families, and the regulatory messages that surround a failed settlement.

This article has been made with the help of Claude Code and several custom skills

[TOC]

What sese does

sese carries the instructions and responses that settle securities. A participant tells its CSD or custodian to deliver or receive a quantity of a security against payment, or free of payment, and the settlement system matches that instruction with the counterparty’s mirror image, holds it until the intended settlement date, and moves the securities and cash. sese is the instruction-and-confirmation language for that process, the active counterpart to the reporting area semt and the downstream end of the clearing area secl.

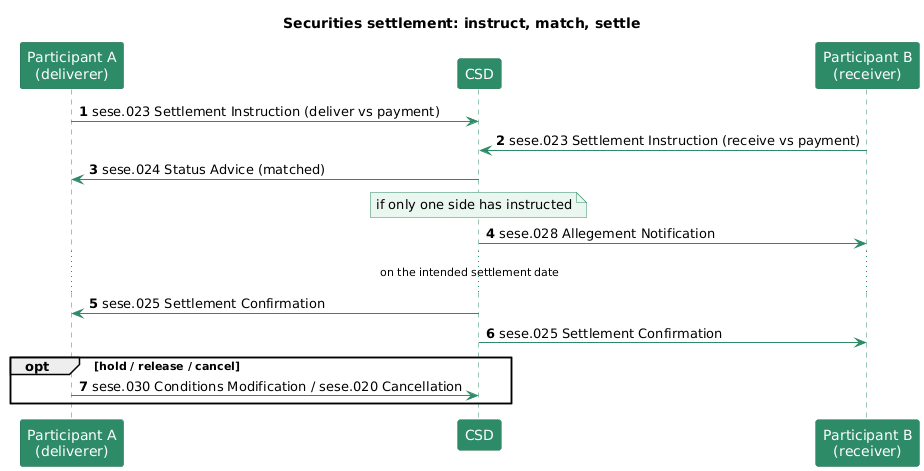

The central mechanism is matching. Settlement is instructed by both sides independently: the deliverer sends an instruction to deliver, the receiver sends one to receive, and the CSD compares them on the key economic terms. Only when they match does the transaction settle. This two-sided design is what makes settlement safe, and it shapes most of the messages in the area.

The settlement instruction

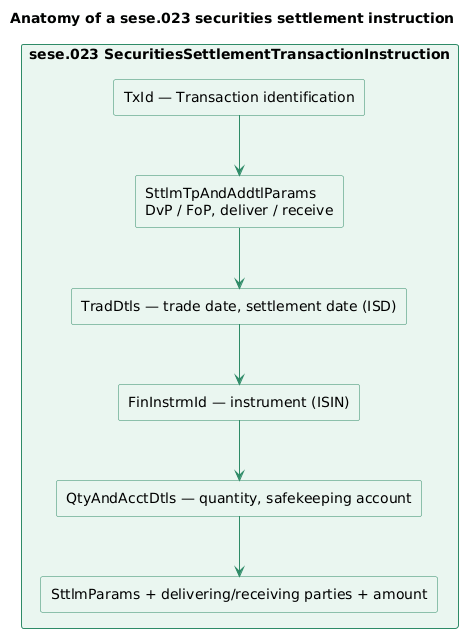

The heart of sese is the sese.023 SecuritiesSettlementTransactionInstruction, the message a participant sends to settle a trade. Its structure names everything the CSD needs to match and settle.

- Transaction identification (

TxId) uniquely names the instruction. - Settlement type and additional parameters (

SttlmTpAndAddtlParams) state whether it is delivery versus payment or free of payment, and whether the participant delivers or receives. - Trade details (

TradDtls) carry the trade date and the intended settlement date. - Financial instrument identification (

FinInstrmId) names the security, normally by ISIN. - Quantity and account details (

QtyAndAcctDtls) give the quantity and the safekeeping account. - Settlement parameters, delivering and receiving parties, and the settlement amount complete the instruction with the settlement conditions and the cash leg.

Delivery versus payment (DvP) is the key idea in those parameters: the securities move only if the cash moves, and vice versa, so neither side is left having given up one without receiving the other. Free of payment (FoP) settles the securities alone, used when cash is handled separately or not at all.

The settlement lifecycle

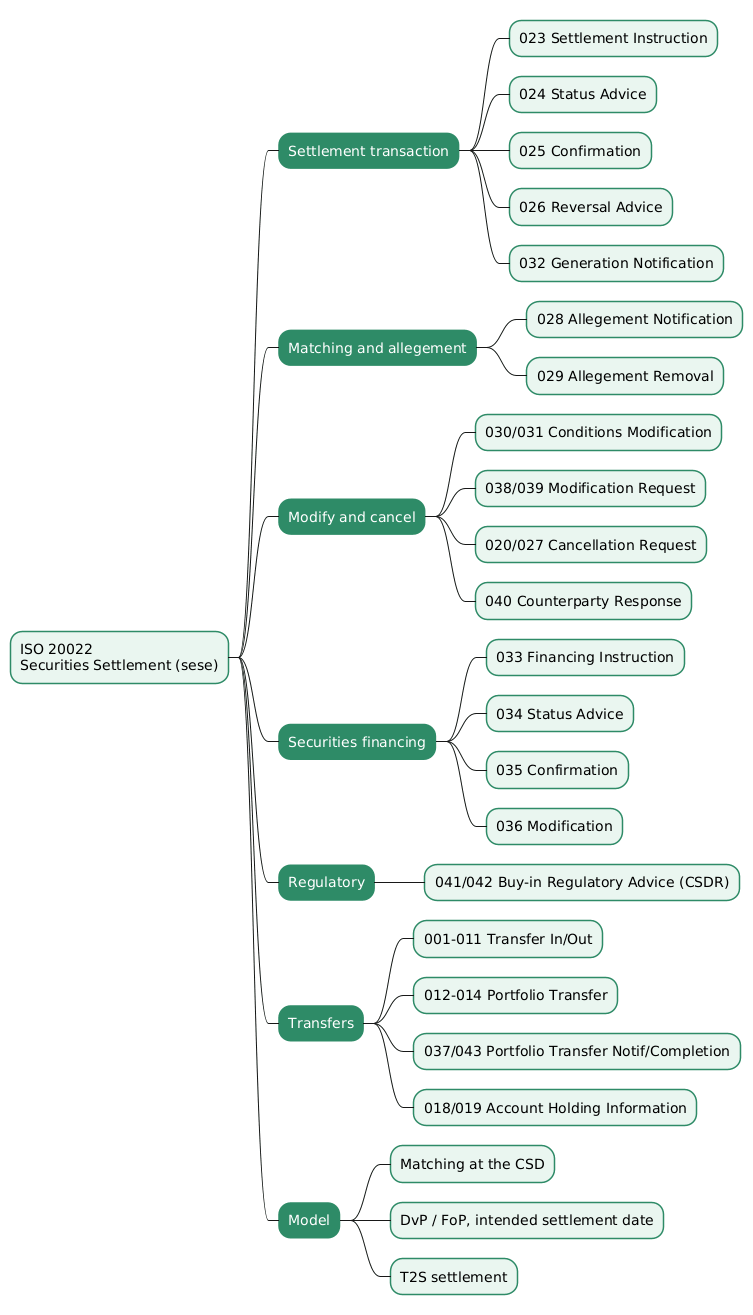

The core messages trace an instruction from submission to settlement.

Instruct and match. Both participants send their sese.023 instructions to the CSD. The CSD reports progress in a sese.024 SecuritiesSettlementTransactionStatusAdvice, which carries the transaction through statuses such as matched, pending, and failing. Where only one side has instructed, the CSD warns the other with a sese.028 SecuritiesSettlementTransactionAllegementNotification, an “someone has instructed a trade against you, please instruct your side” message, withdrawn by a sese.029 allegement removal advice if the alleged trade is dropped.

Settle or reverse. On the intended settlement date, once the transaction is matched and the securities and cash are available, the CSD settles it and reports a sese.025 SecuritiesSettlementTransactionConfirmation to each side. If a settled transaction must later be undone, a sese.026 reversal advice reports the reversal. Some transactions are not instructed by a participant at all but generated by the system, for example from a corporate action or a realignment, and those are announced with a sese.032 generation notification.

Modify and cancel. A matched instruction is not frozen. A participant can change its settlement conditions, for example placing it on hold or releasing it, with a sese.030 conditions modification request answered by a sese.031 status advice; change other details with a sese.038 modification request and its sese.039 advice; or cancel it with a sese.020 cancellation request, tracked by the sese.027 cancellation status advice. Because a cancellation of a matched trade affects both sides, the counterparty’s agreement can be sought, and the sese.040 counterparty response carries it.

Securities financing

Repo and securities-lending transactions settle through their own sese family, because they have two legs (an opening and a closing) rather than one. The sese.033 SecuritiesFinancingInstruction instructs the financing transaction, the sese.034 status advice reports its progress, the sese.035 confirmation confirms settlement, and the sese.036 modification instruction changes it, for example to adjust the closing leg or the rate. The family lets a repo or stock loan be settled and managed with the same rigour as an outright trade.

Transfers

A separate group moves an entire position or portfolio between accounts rather than settling a trade, the machinery behind moving assets from one custodian or fund platform to another.

- Transfer in and out (

sese.001tosese.011) instruct, confirm, cancel, and reverse the transfer of a holding into or out of an account, with status reports for each. - Portfolio transfer (

sese.012tosese.014, plus thesese.037notification andsese.043completion) moves a whole portfolio, coordinating the many individual holdings it contains. - Account holding information (

sese.018,sese.019) requests and provides the list of holdings to be transferred, so the receiving side knows what is coming.

Settlement discipline and buy-in

Settlement fails carry regulatory consequences, and sese includes the messages for one of them. The sese.041 BuyInRegulatoryAdvice and its sese.042 response communicate a regulatory buy-in, the CSDR mechanism under which a persistently failing delivery is closed out by buying the securities in the market at the failing party’s cost. These sit next to the penalty reporting in the semt area to give the settlement-discipline regime its message support.

Conclusion

The sese business area is where a securities trade finally happens. Its core is the sese.023 settlement instruction and the matched lifecycle around it: instruct, match, allege the missing side, modify or cancel, then settle and confirm, or reverse. Around that core sit the securities-financing family for repo and stock lending, the transfer family for moving positions and whole portfolios between accounts, and the buy-in advice that supports the settlement-discipline regime. Read together with the clearing area secl that feeds it, the collateral area colr whose deliveries it performs, and the reporting area semt that describes its results, sese is the settlement engine at the end of the securities post-trade chain.

Annex — Key Terms

| Term | Definition |

|---|---|

| sese | The ISO 20022 securities settlement business area, covering settlement instructions, financing, transfers, and settlement-discipline messages. |

Settlement instruction (sese.023) |

The message instructing a CSD or custodian to deliver or receive a security, carrying the instrument, quantity, account, dates, and parties. |

| Matching | The comparison of the two counterparties’ mirror-image instructions on their key terms, required before a transaction can settle. |

| Delivery versus payment (DvP) | Settlement in which the securities move only if the cash moves, so neither side gives up one leg without the other. |

| Free of payment (FoP) | Settlement of the securities alone, with cash handled separately or not at all. |

| Intended settlement date (ISD) | The date on which a matched transaction is due to settle. |

Allegement (sese.028) |

A notification that a counterparty has instructed a trade against an account whose owner has not yet instructed its side. |

Settlement confirmation (sese.025) |

The message confirming that a transaction has settled, sent to each side. |

Securities financing (sese.033) |

The instruction family for repo and securities-lending transactions, which settle in two legs. |

Regulatory buy-in (sese.041) |

The CSDR mechanism, advised through sese.041/sese.042, that closes out a persistently failing delivery by buying the securities in the market. |

Frequently Asked Questions

Q: Why must a settlement transaction be matched before it settles?

Because settlement is instructed by both sides independently, and matching is the check that they agree. The deliverer sends an instruction to deliver and the receiver one to receive, and the CSD compares them on the key economic terms: the security, the quantity, the settlement date, the amount, and the parties. Only when the two line up does the transaction settle. This two-sided confirmation prevents one participant’s error or unilateral instruction from moving securities and cash that the other side never agreed to.

Q: What does delivery versus payment mean, and where is it set in a sese.023?

Delivery versus payment (DvP) means the securities and the cash move together or not at all: the delivery of securities is conditioned on the payment, and vice versa, so neither party is left having given up its leg without receiving the other. It is set in the settlement type and additional parameters (SttlmTpAndAddtlParams) of the sese.023 instruction, which state whether the transaction is DvP or free of payment and whether the participant delivers or receives. DvP is the mechanism that removes principal risk from settlement.

Q: What is an allegement, and which message carries it?

An allegement is the CSD telling a participant that its counterparty has instructed a trade against the participant’s account, but the participant has not yet instructed its own side. It is effectively a prompt: “someone is expecting you to settle this, please instruct.” It is carried by the sese.028 SecuritiesSettlementTransactionAllegementNotification, and if the alleged trade is later dropped, a sese.029 allegement removal advice withdraws it. Allegements are how a participant learns about a pending settlement it has not yet matched.

Q: How does securities settlement differ from securities financing in sese?

An outright settlement moves securities against cash once, and is handled by the core sese.023 instruction and its lifecycle. A financing transaction, a repo or a securities loan, has two legs: an opening leg that lends the securities or cash and a closing leg that returns them later. Because of that two-legged shape, financing has its own family: sese.033 instructs it, sese.034 reports status, sese.035 confirms, and sese.036 modifies it. The separate family lets the standard capture the opening and closing legs and the financing terms that an outright trade does not have.

Q: How does sese connect to the clearing, collateral, and reporting areas?

sese is the settlement step the others feed into or read from. The clearing area secl ends with a settlement obligation that becomes a sese.023 instruction. The collateral area colr agrees which assets move in a margin call, and their delivery is performed by sese. The reporting area semt then describes the results: a sese.023 instruction still to settle appears on a semt.018 pending report, and a sese.028 allegement appears on a semt.019 allegement report. sese is the engine; the others instruct it, cover it, or report on it.

Q: What regulatory messages does sese include for settlement fails?

It includes the buy-in advice pair. Under the CSDR settlement-discipline regime, a delivery that keeps failing can be closed out by buying the securities in the market at the failing party’s cost, and the sese.041 BuyInRegulatoryAdvice and sese.042 response communicate that regulatory buy-in. They complement the cash penalties reported in the semt area through semt.044, so the two areas together support the fails regime: penalties for the delay and a buy-in to force the delivery.