ISO 20022 for Securities Events — The seev Message Set

- What seev covers

- Corporate actions

- General meetings and proxy voting

- The other sub-domains

- Conclusion

- Annex — Key Terms

- Frequently Asked Questions

- References

Owning a share is not a static thing. The company pays dividends, offers rights, splits its stock, and calls its holders to vote at meetings. Each of these is a securities event, and communicating them down the chain from issuer to investor, then collecting the investors’ choices back up, is what ISO 20022’s seev business area is for. It is a large area, seventy-three messages, because it spans several distinct processes: corporate actions, general meetings and proxy voting, shareholder identification, market claims, and buyer protection. This article maps those sub-domains and follows the corporate-action lifecycle that anchors the area.

This article has been made with the help of Claude Code and several custom skills

[TOC]

What seev covers

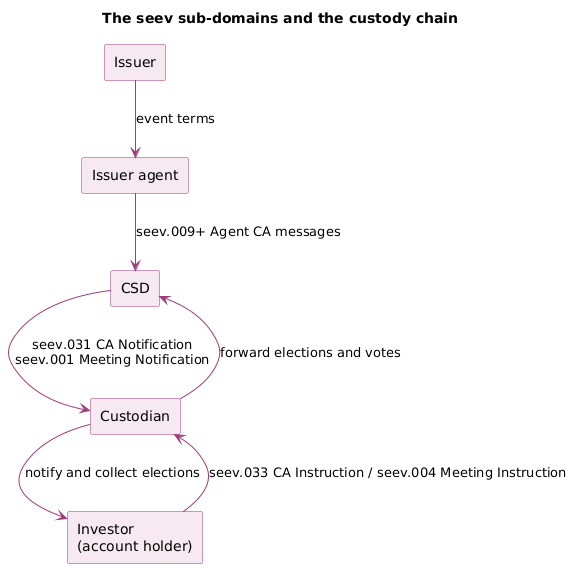

A securities event is anything that happens to an issued security during its life and affects its holders. seev carries these events across the custody chain: from the issuer and its agent, through the central securities depository (CSD), to custodians, and finally to the investors who hold the securities in their accounts. Because the investor is often several intermediaries away from the issuer, the event has to be announced downward and the investor’s response gathered upward, at each link.

The area splits into several processes that share this chain.

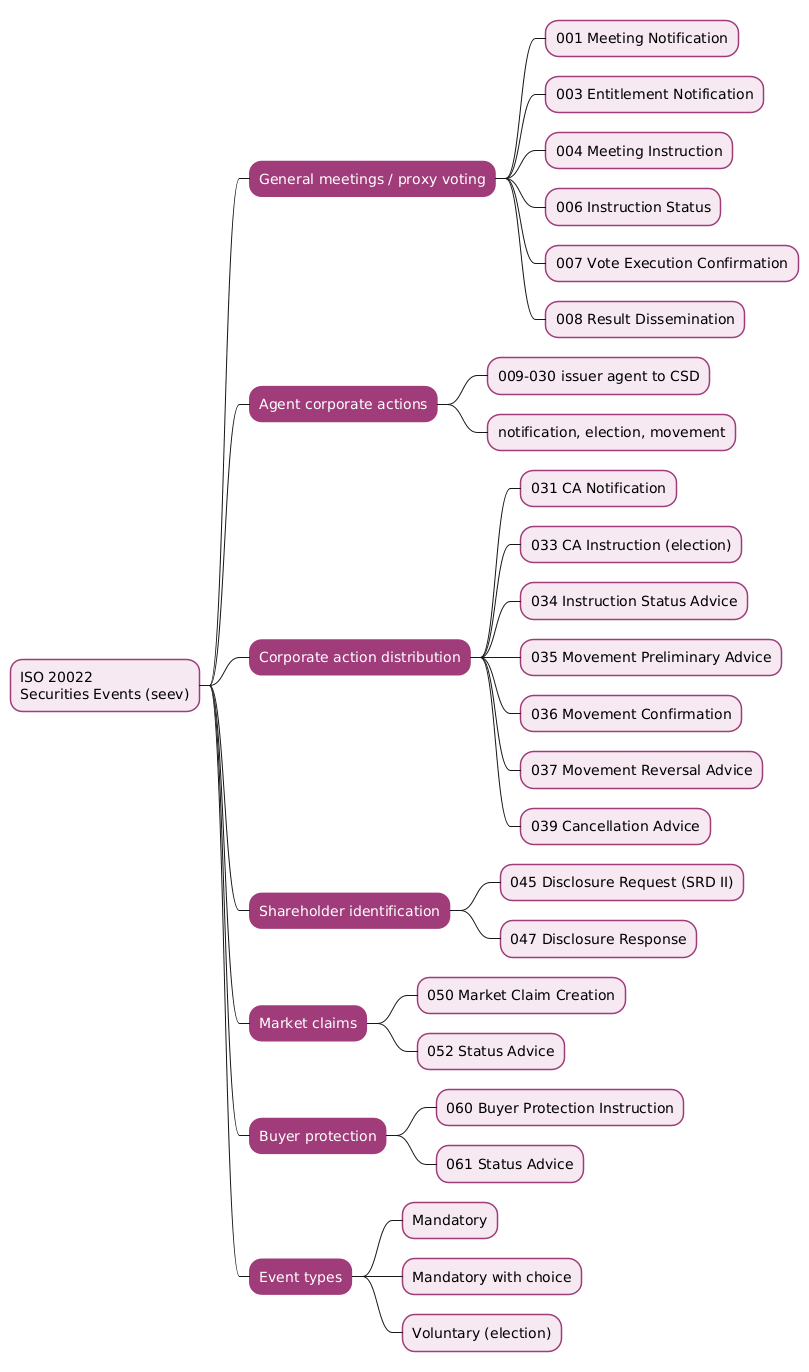

| Sub-domain | Messages | Purpose |

|---|---|---|

| General meetings and proxy voting | seev.001 to seev.008 |

Notify meetings, gather votes, disseminate results |

| Agent corporate actions | seev.009 to seev.030 |

Set up and run a corporate action between issuer agent and CSD |

| Corporate action distribution | seev.031 to seev.044 |

Announce and process corporate actions to account holders |

| Shareholder identification | seev.045 to seev.049 |

Disclose shareholder identity up the chain (SRD II) |

| Market claims | seev.050 to seev.053 |

Compensate entitlements on in-flight trades |

| Buyer protection | seev.060 to seev.067 |

Let a buyer instruct elections before settlement |

Corporate actions

Corporate actions are the largest and most-used part of seev, the messages between an account servicer (a CSD or custodian) and the account holders it serves. Events come in three kinds, and the distinction drives the flow.

- Mandatory events happen automatically, such as a cash dividend or a stock split; the holder receives the outcome without doing anything.

- Mandatory with choice events require the holder to pick from options, with a default if it does not.

- Voluntary events, such as a tender offer or exercising rights, happen only if the holder elects to take part.

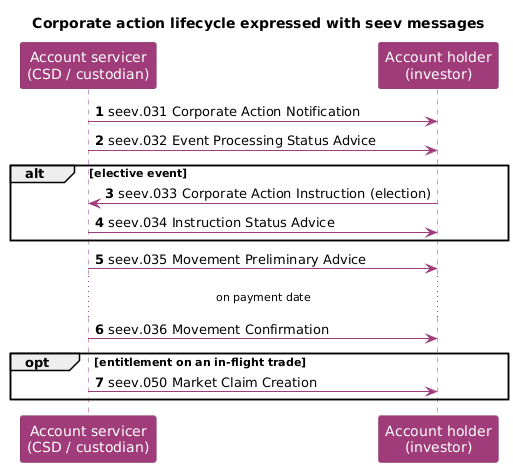

The flagship announcement is the seev.031 CorporateActionNotification, which carries the event: a notification-general-information block, a corporate-action-general-information block giving the event type and its key dates, and the account details of the holder it concerns. Everything else in the corporate-action flow follows from that announcement.

The lifecycle runs as follows. The servicer announces the event with a seev.031 Notification and reports its processing state with a seev.032 EventProcessingStatusAdvice. For an elective event, the holder responds with a seev.033 CorporateActionInstruction carrying its election, and the servicer confirms receipt with a seev.034 InstructionStatusAdvice. As payment approaches, a seev.035 MovementPreliminaryAdvice tells the holder what it is due to receive, and on the payment date a seev.036 MovementConfirmation confirms the securities or cash actually credited. If a booked movement must be undone, a seev.037 MovementReversalAdvice reverses it, and free-text detail that does not fit the structured fields travels in a seev.038 CorporateActionNarrative. Cancellations of an event or of an instruction are handled by seev.039 and seev.040.

General meetings and proxy voting

The first eight messages handle the shareholder’s other main right: voting. A seev.001 MeetingNotification announces a general meeting and its agenda, a seev.003 MeetingEntitlementNotification tells a holder how many votes it may cast, and the holder instructs its votes with a seev.004 MeetingInstruction. The servicer reports progress with a seev.006 MeetingInstructionStatus, confirms the votes were lodged with a seev.007 MeetingVoteExecutionConfirmation, and, after the meeting, circulates the outcome with a seev.008 MeetingResultDissemination. This is the proxy-voting chain that lets an investor several custodians removed from the issuer still vote its shares.

The other sub-domains

Three further processes round out the area.

- Shareholder identification disclosure (

seev.045toseev.049) implements the transparency an issuer is entitled to under rules such as the EU Shareholder Rights Directive II: aseev.045disclosure request travels down the chain andseev.047responses return the identities of the underlying holders. - Market claims (

seev.050toseev.053) handle entitlements on trades that were in flight over a corporate action’s record date. Aseev.050MarketClaimCreation raises a claim so the party that should have received a dividend or other benefit is compensated, even though the trade had not yet settled. - Buyer protection (

seev.060toseev.067) lets the buyer of a security involved in an elective event give its election before the trade settles, through aseev.060BuyerProtectionInstruction, so it does not lose the right to choose because settlement is late.

Conclusion

The seev business area carries the events in the life of a security across the custody chain. Its seventy-three messages cover corporate actions, from the seev.031 notification through elections to the movement confirmation that pays them, general meetings and the proxy-voting chain that lets distant investors vote, shareholder identification for issuer transparency, market claims that compensate entitlements on unsettled trades, and buyer protection for elective events in flight. What ties them together is direction: an event is announced downward from issuer to investor, and the investor’s choice, an election or a vote, is gathered back upward. Read next to the settlement area sese that moves the resulting securities and cash, seev is how a security’s corporate life reaches the people who own it.

Annex — Key Terms

| Term | Definition |

|---|---|

| seev | The ISO 20022 securities events business area, covering corporate actions, meetings, shareholder identification, market claims, and buyer protection across seventy-three messages. |

| Corporate action | An event affecting a security’s holders, such as a dividend, split, rights issue, or tender offer. |

| Mandatory event | A corporate action that happens automatically, with no choice required from the holder. |

| Voluntary event | A corporate action that occurs only if the holder elects to take part. |

Corporate action notification (seev.031) |

The announcement of a corporate action, carrying the event type, key dates, and affected account. |

Corporate action instruction (seev.033) |

The holder’s election in response to an elective event. |

Movement confirmation (seev.036) |

The message confirming the securities or cash actually credited on the payment date. |

| Proxy voting | The process by which an investor casts votes at a general meeting through the custody chain, using the seev.001 to seev.008 messages. |

| Market claim | A compensation for an entitlement on a trade that was unsettled over a corporate action’s record date, raised by seev.050. |

| Buyer protection | The mechanism (seev.060) letting a buyer instruct its election on an elective event before the trade settles. |

Frequently Asked Questions

Q: What are the three kinds of corporate action, and how do they differ?

Mandatory, mandatory with choice, and voluntary. A mandatory event, such as a cash dividend or a stock split, happens automatically and the holder simply receives the outcome. A mandatory-with-choice event requires the holder to pick from options but applies a default if it does not respond. A voluntary event, such as a tender offer or the exercise of rights, happens only if the holder actively elects to take part. The distinction matters because elective events need the holder to send a seev.033 instruction, while a purely mandatory event needs no response.

Q: Why does a securities event have to travel through a chain of intermediaries?

Because the investor usually does not hold its securities directly with the issuer. Its holding sits with a custodian, which holds with another custodian or a CSD, which connects to the issuer’s agent. When an event occurs, the announcement has to pass down this chain from the issuer to the investor, and the investor’s response (an election or a vote) has to pass back up. seev provides messages for each link, which is why the corporate-action distribution and agent-corporate-action sub-domains both exist: they carry the same event at different points in the chain.

Q: What is the corporate-action lifecycle in seev messages?

It begins with a seev.031 CorporateActionNotification announcing the event and a seev.032 status advice on its processing. For an elective event, the holder sends a seev.033 instruction with its election and receives a seev.034 status advice. Before payment, a seev.035 movement preliminary advice states what the holder is due, and on the payment date a seev.036 movement confirmation records what was actually credited. A seev.037 reversal advice can undo a booked movement, and cancellations are handled by seev.039 and seev.040. The arc runs from announcement, through election where needed, to the confirmed payment.

Q: What problem do market claims solve?

They solve who gets an entitlement when a trade is unsettled over a corporate action’s record date. If you buy shares just before a dividend record date but the trade has not settled by then, the dividend is paid to the seller who is still the holder of record, even though you are economically entitled to it. A market claim corrects this: a seev.050 MarketClaimCreation raises a claim so the benefit is passed to the party that should have received it. Buyer protection (seev.060) addresses a related timing problem for elective events, letting a buyer instruct its election before its trade settles.

Q: How does shareholder identification in seev relate to regulation?

The shareholder-identification messages (seev.045 to seev.049) implement an issuer’s right to know who its shareholders are, a right strengthened in the EU by the Shareholder Rights Directive II. Because holdings are layered through intermediaries, an issuer cannot see the underlying investors directly. A seev.045 disclosure request travels down the custody chain and seev.047 responses return the identities back up, so the issuer can assemble a picture of its beneficial owners. It is an example of regulation driving a dedicated sub-domain into an ISO 20022 business area.

Q: How does seev connect to sese?

They handle different halves of a corporate action’s effect. seev announces the event and gathers the holder’s choice; sese moves the securities and cash that result. When a seev.036 movement confirmation reports that a holder has been credited with new shares or cash, the underlying movement is a settlement handled in the sese area. In short, seev decides what should happen to a holding because of an event, and sese performs the resulting transfer.